A new analysis by real estate company Zoocasa highlights the stark reality of homeownership in Canada, showing that today’s buyers face far greater financial burdens than those of previous generations, despite lower interest rates and rising incomes.

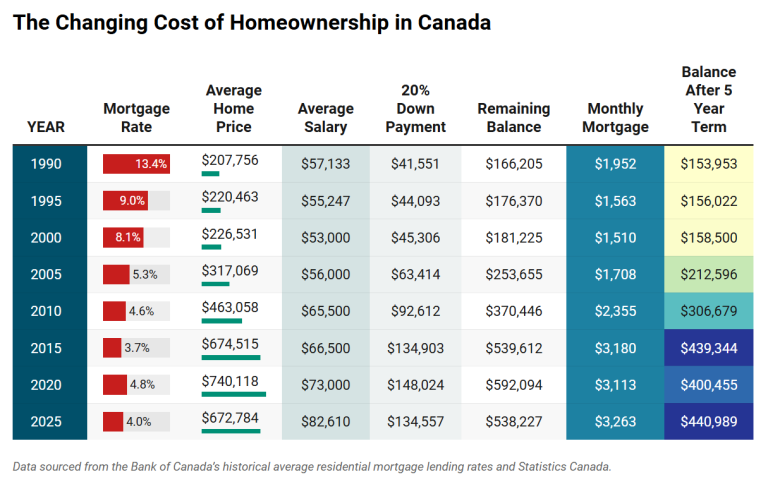

In 1990, the average Canadian home cost $207,756. With a 20 per cent down payment of $41,551, the remaining mortgage of $166,205 carried an interest rate of 13.4 per cent. This translated to monthly payments of $1,952, consuming 41 per cent of a typical family’s $57,133 after-tax income.

By contrast, in 2025 the average home price has surged to $672,784, requiring a down payment of $134,557 and leaving buyers with a $538,227 mortgage. Even at a comparatively modest interest rate of 4.04 per cent, monthly payments rise to $3,263 — nearly half (47 per cent) of a family’s $82,610 after-tax income.

“Couples today carry mortgages three times larger than those of 1990 while dedicating a larger share of their paycheques to service them,” Zoocasa noted, adding that “income growth has not kept pace with home prices, and affordability has deteriorated despite lower interest rates.”

The report also reveals that saving for a down payment has become significantly more difficult. In 1990, households could typically save for a down payment in about 10 years at a 7.2 per cent savings rate. Today, the same effort takes 22 years, pushing many millennials and Gen Z buyers into delaying homeownership until their 40s without external assistance.

Equity growth has also slowed. Homeowners in 1990 reduced their mortgage principal much more quickly, while buyers today remain heavily indebted well into midlife, leaving them vulnerable to market downturns and limiting their ability to use their homes for wealth-building.

Generational differences are stark:

- Boomers benefited from falling rates after buying relatively affordable homes in the late 1980s and early 1990s, building equity quickly.

- Gen X balanced rising prices with falling interest rates between the late 1990s and early 2010s.

- Millennials faced record-high prices despite historically low borrowing costs, delaying entry into the market.

- Gen Z faces the steepest climb yet — with mortgage balances approaching half a million dollars, saving timelines over two decades, and slower equity growth.

These pressures have contributed to declining homeownership rates. National ownership has dropped from 69 per cent in 2011 to 66.5 per cent in 2021. In Ontario, rates fell from 71.4 per cent to 68.4 per cent over the same period.

Zoocasa’s findings underscore the widening gap between past and present generations in achieving homeownership, with affordability challenges now shaping the financial futures of younger Canadians.